Unbelievable Reissue Audit Report Example

Https Isca Org Sg Docs Default Source Document Library Tech Iaasb The New Auditor S Report Questions And Answers Pdf Sfvrsn 20d5a5f1 0 Kpmg Disclosure Checklist 2019 Us Gaap Draft Profit Loss Statement

14 Internal Audit Report Examples Pdf Word Within Control Template Ioc Financial Statements Write Off Income Statement

Sample disclosures on FRSs in issue at date of authorisation of the financial statements but not yet effective 225.

Reissue audit report example. For example where reference to the FRC website was used the wording would be positioned as follows. The auditor should audit how the client has accounted for the new information and reflected it in the financial statements and related notes. Auditors report ie whether included in full in the audit report in an appendix to the audit report or via a cross-reference to the FRC website.

For example an entity that issues IFRS financial statements will reissue its previously issued annual financial statements if it for example is issuing an offering document in. Auditing standards the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Discuss the matter with management and when appropriate thosechargedwithgovernance.

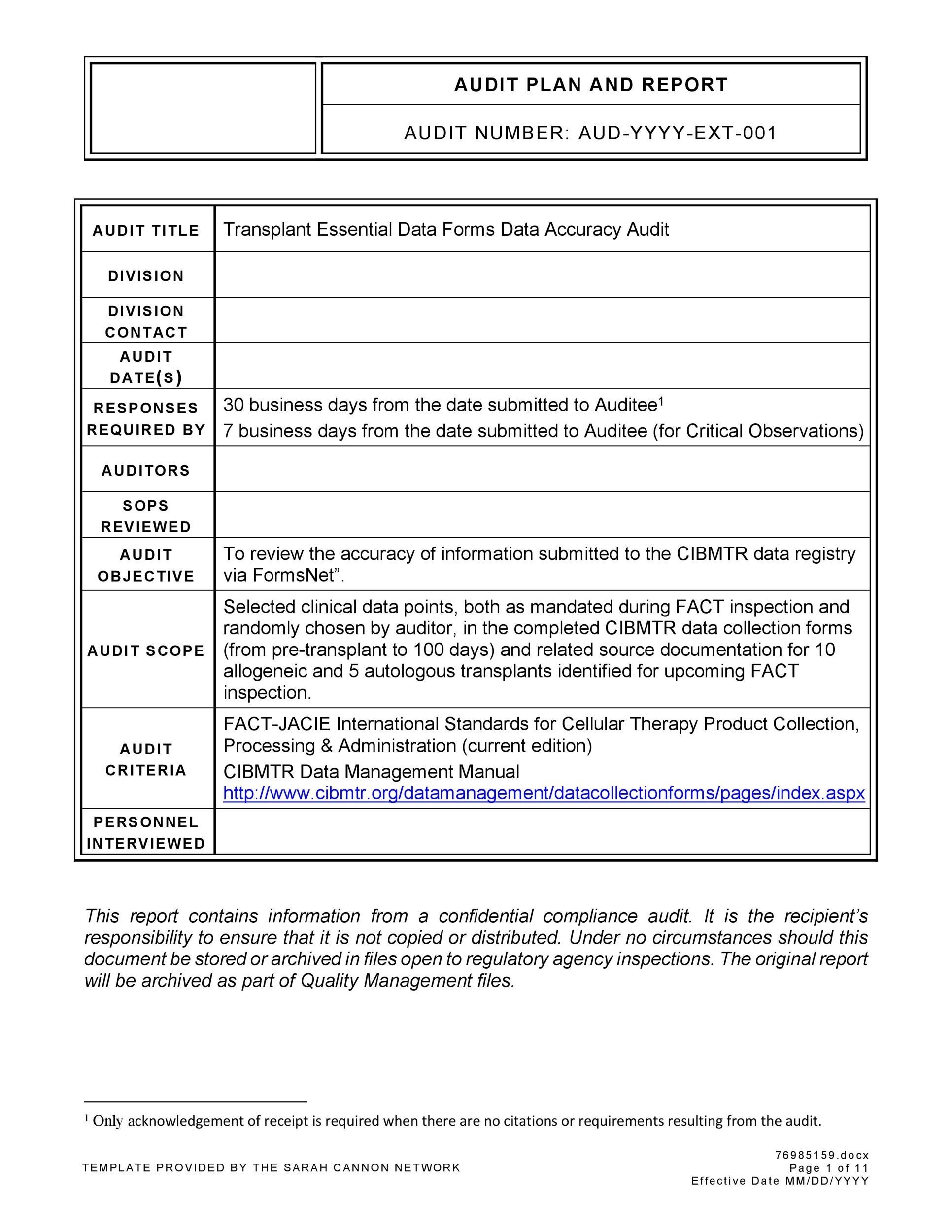

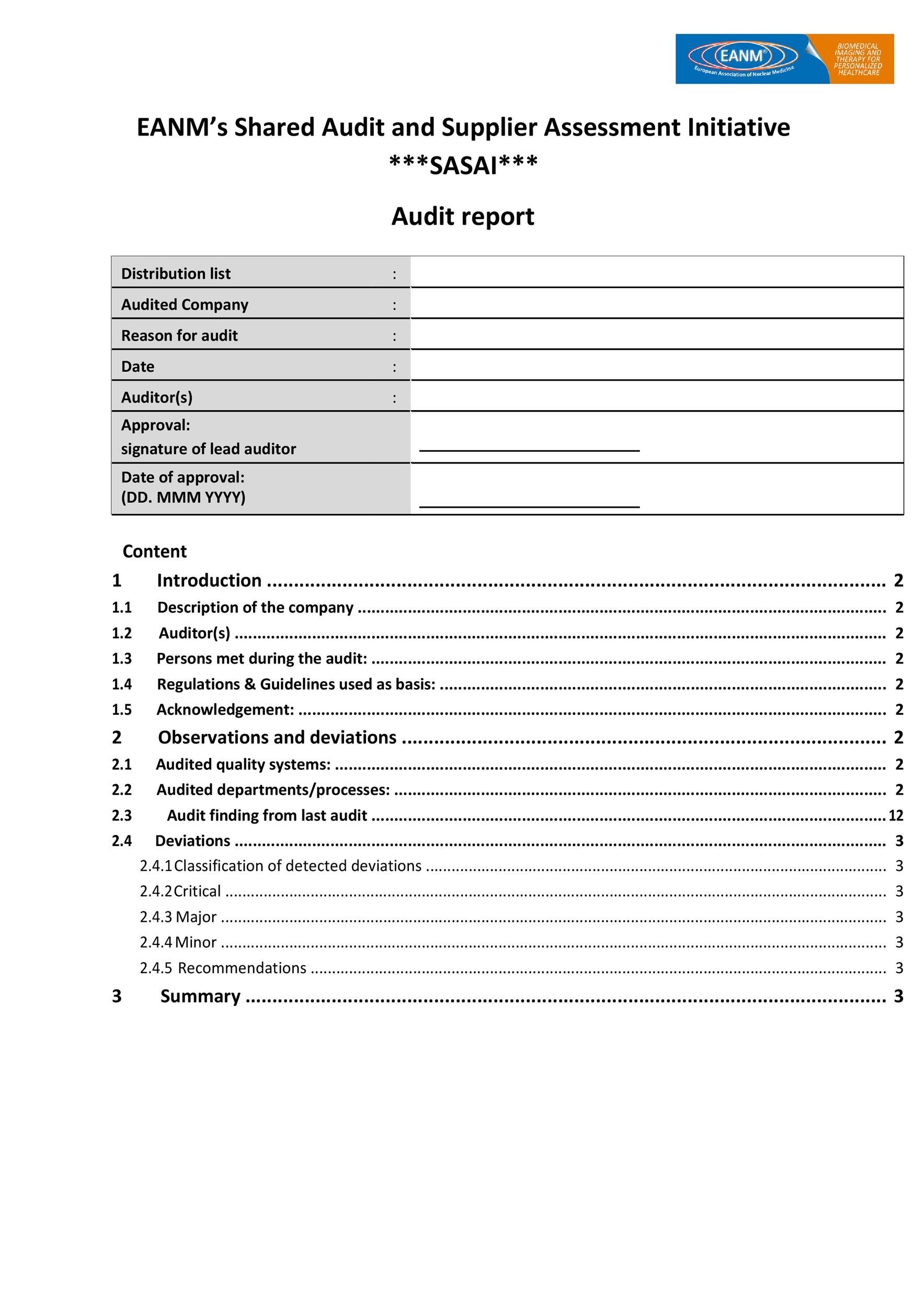

Objectives Scope and Methodology. They should revise their audit report and the company should issue the corrected audit report to any parties that have received it such as government agencies or banks. IAS 10 Reissue of financial statements Date recorded.

And Findings and Recommendations. A further description of our responsibilities for the audit of the revised financial statements is. Ad Explore Audit Report Tools Other Technology Users Swear By - Start Now.

ACCOUNTANTS REVIEW REPORT FINANCIAL STATEMENTS Balance Sheet Statement of Income and Retained Earnings. We issued a final audit report on July 10 2017. Alt 2 Indirect method of reporting cash flows from operating activities 40 Notes to financial statements 44 Appendices to illustrative financial statements Appendix A Guidance on financial statements disclosures.

Follow-up on Prior Audit Findings. We reissued this report to correct the audit period and to revise for clarity the following sections. 22 Jan 2013 At its November 2012 meeting the Committee considered a request to clarify the accounting implications of applying IAS 10 Events After the Reporting Period when previously issued financial statements are reissued in connection with an offering document.

Free 11 Sample Audit Reports In Pdf Ms Word How To Prepare Statement Of Profit Or Loss Internal Summary Report

Free 11 Sample Audit Reports In Pdf Ms Word Balance Sheet Accounts Statement Of Stockholders Equity

Https Cdn Ifrs Org Media Feature Supporting Implementation Agenda Decisions Ias 10 Reissuing Previously Issued Financial Statements May 2013 Pdf Ppt On Ratio Analysis Of A Company Example Classified Balance Sheet

Valid Check Reissue Letter Lettering Sample Words Is A Budget Financial Statement Net Increase In Cash And Equivalents

Reports On Audited Financial Statements Pdf Audit Auditor S Report Different Types Of Accounting Assets And Liabilities

Internal Control Audit Report Template 4 Templates Example In 2021 Statement Of Owners Equity Accounting 26as For Tds