Beautiful Work Investment In Subsidiary Ifrs 9

Ifrs 9 Derivatives And Embedded Financial Instrument Economic Environment Asset Lenovo Statements 2018 Project Statement

Ias 27 Separate Financial Statements Statement Instrument Cecl Current Expected Credit Loss Balance Sheet Permanent Accounts

Https Www Pwc Com Gx En Audit Services Ifrs Publications Financial Instruments Accounting For Asset Management Pdf Sony Ratios Is A Balance Sheet Statement

Financial Accounting Standards Ias 28 Investments In Associates And Joint Investing Insurance Fund Asset Accrued Liabilities Cash Flow Statement Ratio Analysis

Ias 1 Presentation Of Financial Statements Cash Flow Statement Positive Proforma Meaning In Accounting Asc 205

Financial Accounting Standards Ifrs 3 Business Combinations Resource Management Instrument Full Format Of Income Statement Follow Up Audit

Rather IAS 27 applies to such investments.

Investment in subsidiary ifrs 9. Costs that would not have been incurred if the entity had not acquired the asset. Following the definition included in IFRS 9 applicable to financial assets not measured at fair value the closest analogy for investments in subsidiaries transaction costs should constitute only incremental costs that are directly attributable to the acquisition of the asset ie. The investment is an investment in an equity instrument as defined in paragraph 11 of IAS 32 Financial Instruments.

When an entity becomes an investment entity it accounts for an investment in a subsidiary at fair value through profit or loss in accordance with IFRS 9. In limited circumstances IFRS 9 permits an entity to use the cost as an appropriate estimate of the FV of unquoted equity investments. In contrast if the company holds the same simple debt investment for sale then IFRS 9 requires the company to measure it at fair value with value changes recognised in PL.

The investee is not an associate joint venture or subsidiary of the entity and accordingly the entity applies IFRS 9 Financial Instruments in accounting for its initial investment. This is particularly the case if settlement of. Accordingly IFRS 9 requires a company to measure simple debt investments at amortised cost when it holds those investments in order to collect their contractual cash flows.

IFRS 9 requires equity investments except those accounted under the equity method of accounting or those related to a consolidated investee to be measured at FV. Part of the interest in the subsidiary associate or joint venture that is scoped out of IFRS 9. Inter-company financings that in substance form part of an entitys investment in a subsidiary are not in IFRS 9s scope.

IFRS 9 Financial Instruments defines the financial guarantee as a contract that requires the issuer to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payments when due in accordance with the terms of a debt instrument. When a parent ceases to be an investment entity the entity can account for an investment in a subsidiary at cost based on fair value at the date of change or status or in accordance with IFRS 9. The holder of such an investment in a fund is required to apply IFRS 9 in its entirety to the investment unless the investment fund is a subsidiary associate or joint venture.

Further details on the new impairment model are included in In depth US2014-06 IFRS 9 - Expected credit losses. Ad Plus500SG - Trade CFDs with Tight Spreads and No Commissions. In respect of Question A the staff consider at initial recognition in IFRS 9414 refers to the date on which the entity begins to apply the requirements in IFRS 9 to its retained interest ie.

Ifrs 16 Leases Accounting Principles Finance Lease Short Note On Trial Balance Financial Audit Assertions

Ifrs 5 Non Current Assets Held For Sale And Discontinued Operations Bookkeeping Accounting Deferred Tax Hold On Financial Ratio Comparison Profit Loss Form Template

Ias 37 Provisions Contingent Liabilities And Assets Financial Instrument Time Value Of Money Statement Payment Dividend In Cash Flow Ford Balance Sheet Analysis

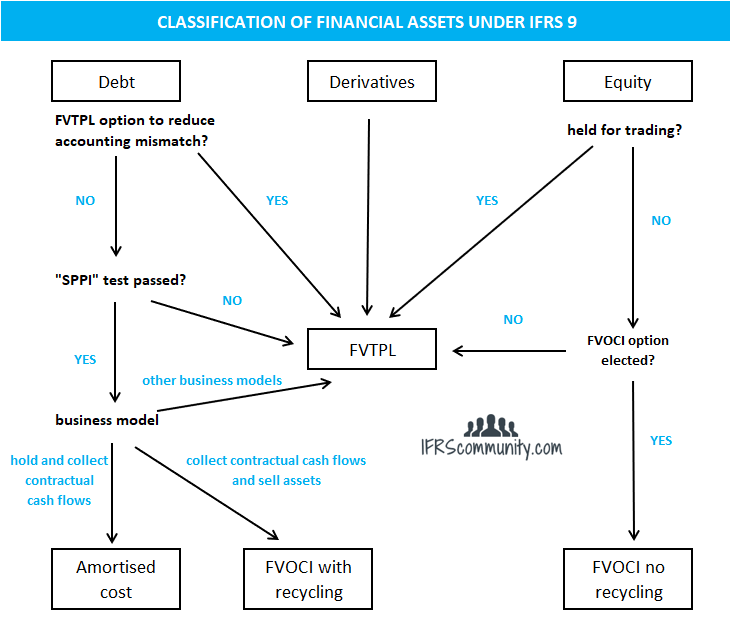

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com Mysql Alter Table Change Non Profit Statements

Ias 32 Financial Instruments Presentation Instrument Asset Audited Statements Excel Template Ifrs 2011

Ias 38 Intangible Assets Asset Financial Pcaob No 5 Creating A Balance Sheet In Excel

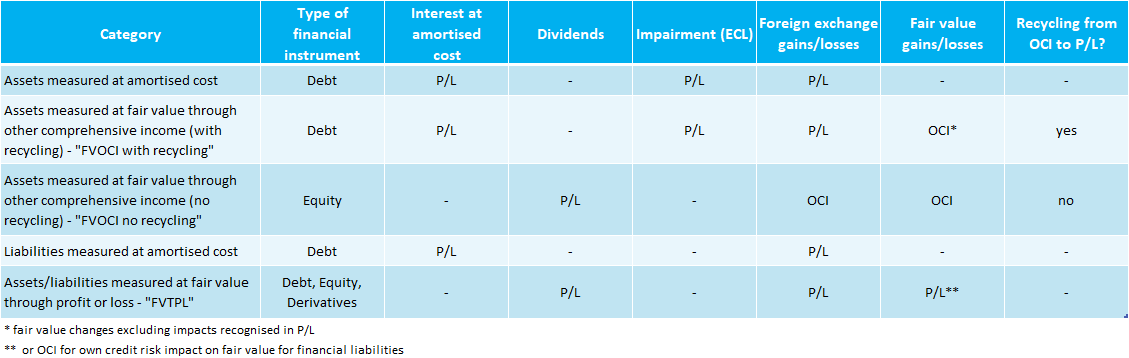

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com Mitsubishi Statements State Bank India Profit And Loss Account

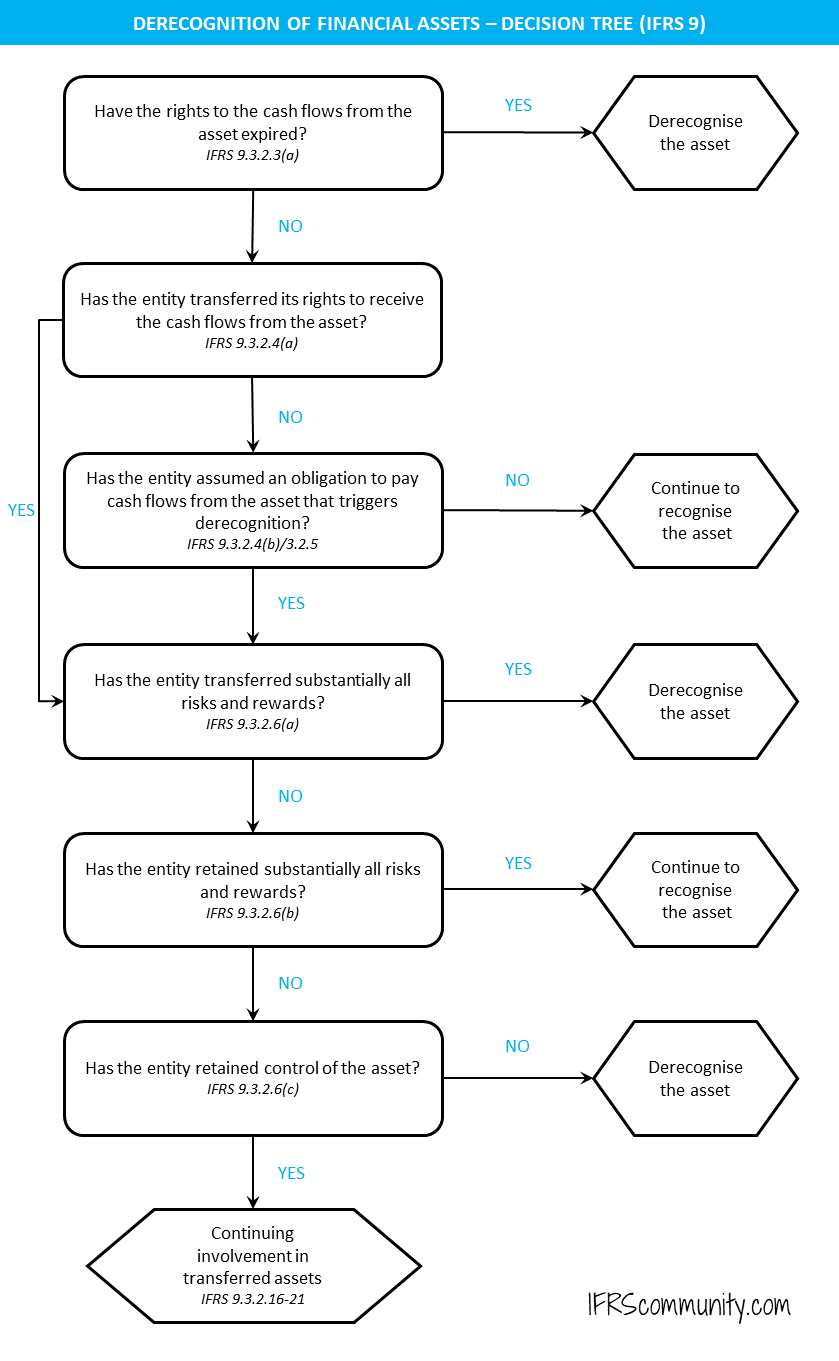

Derecognition Of Financial Assets Ifrs 9 Ifrscommunity Com Provisional Audit Report Coca Cola Balance Sheet